Investment Opportunity Strong, But a Bit Risky, in K-12 Education, Report Says

For investors with an eye on K-12 education as a market, it can be a risky business despite its large size and projected growth.

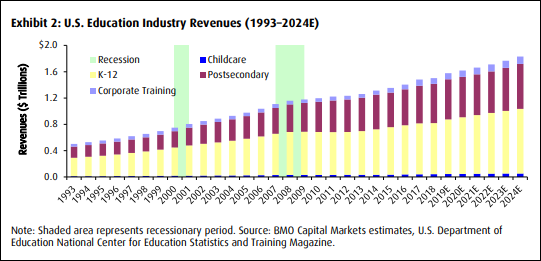

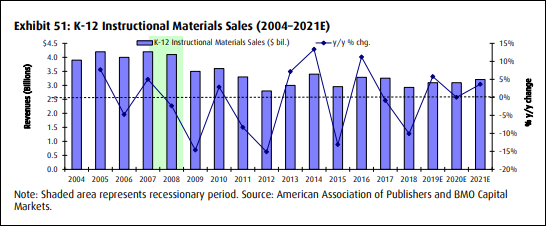

The entire education industry in the United States is expected to grow at an average 3 percent annual rate through 2024, according to BMO Capital Markets, and as the largest segment of that market, K-12 is likely to grow apace in coming years. Sales of instructional materials to schools and districts are also expected to pick up a bit. (See the second chart below.)

In 2019, about $1.58 trillion will be spent in the U.S. on educational services for preschools, K-12, postsecondary and corporate training. Of that amount, the largest part of the education pie—nearly 53 percent, or $830 billion—will be spent in K-12 this year, based on BMO’s analysis from the National Center for Education Statistics. This includes all of the expenditures associated with public and private K-12 schools.

Investors interested in K-12 often look at the market’s size to gauge their potential return on investment, but that doesn’t tell the whole story. “Today, there’s increased pressure on learning outcomes,” said Jeffrey Silber, a stock analyst for education who co-authored BMO Capital Markets‘ “The Education Industry: 2019” report, in an interview. “When you talk to investors, they’re already looking for revenue growth and margin expansion or profit expansion,” he said.

Companies that focus on outcomes first are meeting market demands, he said. “Then hopefully you get revenue growth and profitability,” he said.

Additional drivers in the K-12 market are the growth of blended learning, international demand for education, and the greater use of technology, the report’s authors noted.

While they are generally “bullish” on the long-term prospects for the education market, and foresee steady but modest growth in K-12, there are cautionary notes. Budgetary constraints, regulations, and the need to show academic improvement are among them.

Two recessions slowed the growth of the education industry over the past two decades, and the K-12 part of the industry stands to be adversely impacted in the event of a near-term recession, the report indicated. Solid economic growth will avert that. (See chart below.)

Adding to the complexity of the K-12 market are variables like long sales cycles in districts, the dependence on government spending, and a vulnerability to political pressures.

Some entrepreneurs and investors are attracted to the market because of “the social aspect of this sector: you can do well while doing good,” he said.

Projected K-12 Instructional Materials’ Sales

BMO Capital Markets used market data from the American Association of Publishers and states’ proposed adoption cycles of instructional materials to make projections for growth in this area. For instance, late in 2018 Texas released its list of the latest instructional materials to meet its standards.

The BMO analysts predict increases in net sales for 2019-2021, topping out at $3.2 billion in 2021—still well below the peak sales period from 2004 to 2008.

The chart below shows how K-12 instructional materials’ sales dropped off after the most recent recession, when state adoptions were sluggish, but are expected to edge up.

Technology is another area that is spurring growth, although technology by itself is not the answer to improving student outcomes, said Silber.

The report cites research from three other market sources about the global ed-tech industry, which puts the compound annual growth rate at between 12 percent and 15.4 percent between 2018 and 2024 or 2025.

The full report, which has not been released online yet, is available by emailing Jeff Silber at jeff.silber@bmo.com.

Follow EdWeek Market Brief on Twitter @EdMarketBrief or connect with us on LinkedIn.

See also:

- Ed-Tech Investors Size Up K-12 Market, Advise Entrepreneurs

- Texas, a Prized K-12 Market, Approves Wave of Instructional Materials

- Shifts in California, Texas Markets Create New Dynamics for K-12 Companies

- Inside California’s ELA Adoption: District Buying Patterns

- Florida’s K-12 Market Altered by State Lawmakers, and Huge Storm