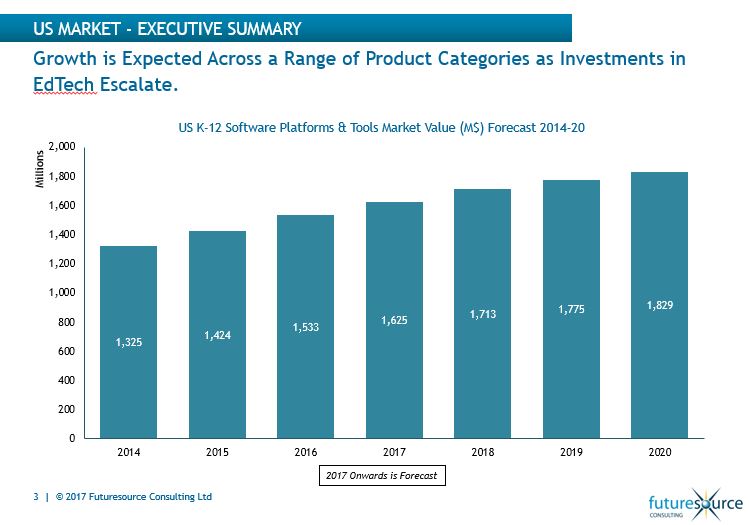

K-12 Ed-Tech Platform and Tools Market Value to Increase to $1.83 Billion by 2020, Report Says

As more computing devices are available in K-12 classrooms, the market for ed-tech software and tools and back-end administrative technology platforms, is expected to grow to $1.83 billion by 2020, according to Futuresource Consulting, Ltd. Data analytics and instructional tools are categories the company predicts will show strong growth.

This year alone, the London-based market research and forecasting company expects U.S. ed-tech and technology in these categories to see a 6 percent increase in market value compared to last year, according to a report the company released recently.

The compound annual growth rate from 2014 to 2020 for all ed-tech and technology is projected to be 4.5 percent, Futuresource’s researchers calculated.

However, year-over-year growth is slowing from increases of about 7.5 percent annually in the first two years of the study to about 5.4 percent each year in 2018 and 2019. By 2020, the year-over-year growth in market value across a range of product categories is expected to be 3 percent, according to the report called “Digital Platforms and Tools in Education: A Review of the K-12 Market in the U.S. and U.K.”

“There are limits to growth,” said Ben Davis, a senior market analyst at Futuresource and co-author of the report with Mike Fisher, the associate director of educational technology. “There are only so many schools—and this number is obviously not increasing that quickly—so as the penetration of these solutions rises, the rate of growth will decline,” he said of the analysis, which was based on initial implementation and licensing costs only. Revenues for additional professional development were not included.

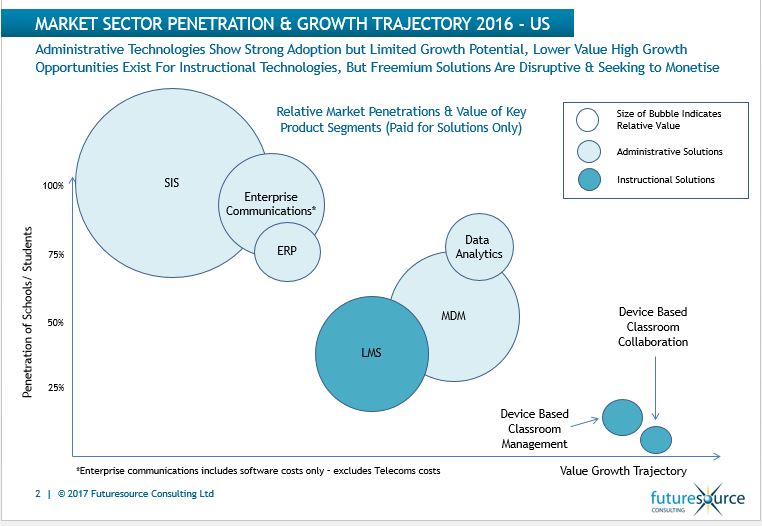

Futuresource created a chart showing the market penetration of different types of technology, with most schools already using student information systems (SIS) and communications platforms that manage voice, email, text and web communications with parents. Enterprise resource planning (ERP) providers address districts’ finance and human resources needs.

“We are seeing bigger enterprise providers, like Oracle SAP that serve other government applications, focusing more on bigger school districts that have more advanced, more customized solutions for HR especially,” Davis said. In the smaller districts, the SIS providers like Skyward, SunGard K-12 (purchased by PowerSchool earlier this year) and Tyler Technologies, offer solutions custom-built for them, he said.

Ed-Tech Growth Opportunities

Futuresource predicts that instructional tools offer strong growth potential, in product segments like LMSs, classroom management and collaboration tools, and student monitoring.

“These tools will become a bigger piece of the pie over time, but there is a lot of competition here, and a lot of price competition from companies like Instructure” trying to gain market share, and freemium solutions like Google Classroom, Class Dojo, Kahoot! and many others.

With the U.S. registering more computer devices in schools than anywhere else in the world, device management is an emerging need that is currently being addressed by companies like Hapara and GoGuardian, Davis said. Futuresource predicts that this segment will grow 10 to 15 percent through 2020.

While LMSs—which have widespread adoption in the U.K.—are expected to become more prevalent in the U.S., Fisher said competing tools that allow teachers to assign work and do other functions an LMS provides, and that are offered under a “freemium” model, pose a threat to the value of this market. Products offered under freemium pricing strategies allow educators to use a tool for free, but teachers or schools must pay if they want to use additional features.

Meanwhile, student information systems from large companies like West and PowerSchool are expanding their core offerings into complimentary solutions and adjacent product categories to continue growing, the report said. After making several acquisitions in recent years, companies like West and Blackboard, which is known for its LMS, “are looking at new markets like social media management tools for safeguarding and monitoring communications, and web applications for the same purposes as well,” said Davis, who explained that the methodology used for the study was primarily interviews with suppliers to get their perspective on product trends, average costs, the competitive landscape, data sharing, and their expectations going forward.

Data Analytics on the Rise

Enterprise-level data analytics are “growing quite rapidly at the moment,” he said. Bigger districts may be using Tableau or Microsoft, while smaller schools might be using BrightBytes or Schoolzilla.

“Traditionally, the market’s been a lot more focused on compliance, reporting on assessment results that have to be sent to the state level,” said Davis. “It’s only been the bigger districts that have some sort of in-house business intelligence that might be doing work looking at outcomes, rather than just reporting back on those outcomes.”

Companies like BrightBytes have started to assess the impact of that technology, he said, and create recommendations for school leaders about any issues the data turn up.

On the financial side, Allovue is an example of a company that raises the same kind of awareness for school leaders by analyzing their budgets and spending, he said.

See also:

- Market for PCs in the U.S. is Growing, But Global Sales Take a Hit

- Ed-Tech Surges Internationally—and Choices for Schools Become More Confusing

- Investors See Promise in Ed-Tech Sector Despite Challenges

- K-12 Dealmaking: PowerSchool to Acquire SunGard’s K-12 Business; India’s Ed. Companies Make Moves

- K-12 Dealmaking: PowerSchool Acquires Chalkable; Edlio Raises $40 Million

- K-12 Dealmaking: PowerSchool Acquires SRB Education Solutions; VIP Kids

Glad you like it. We have been using this for several weeks now and it seems to be going nicely. I also have this same question and i cannot find any proper answers on the internet and also here. need solution. This works really well for us, thank you!

chloraquine https://chloroquineorigin.com/# hcq medical abbreviation