Global K-12 Market for Personal PCs to Contract in 2016, Experts Project

A decline in personal computer sales in the worldwide K-12 education market may be linked to faltering economies in other countries, particularly Latin America, a new report finds.

The total volume of PC sales in that market fell by 12 percent in the first half of 2016, compared to the same period in 2015, despite solid numbers in the U.S. market, according to a report from Futuresource Consulting, a London-based market research firm. The majority of the global decline is attributable to strong economic headwinds in Latin America, caused largely by declining oil prices and political instability. (Similar forces are said to contribute to a tightening in the global, self-paced e-learning market.)

In the United States, the outlook is somewhat rosier. According to Futuresource, volumes in the first half of 2016 increased to 6.4 million shipments from 5.7 million during the same period last year.

While the rate of growth is lower than in 2014 and 2015—when the market was fueled by a national trend away from paper and pencil and toward online assessments—lower average selling prices and a replacement market for outdated devices continue to drive volume, according to a release issued by the consulting firm.

Mike Fisher, associate director of education technology at Futuresource, said that the U.S. market is performing “better than we thought it would,” although declining price points are putting margins under strain for vendors.

The shift to the entry-level side of the market—cash-strapped districts have much greater selection among Chromebooks priced around $150—is mitigated somewhat by the installation, server-hosting, and technical assistance services vendors sell along with each device. But the concern is still there, says Fisher, with some vendors asking, “How low can this go?”

In fact, devices priced at under $200 accounted for 19.1 percent of units sold in the second quarter of 2016, up from 6.3 percent in all of 2015 and only 0.2 percent in 2014.

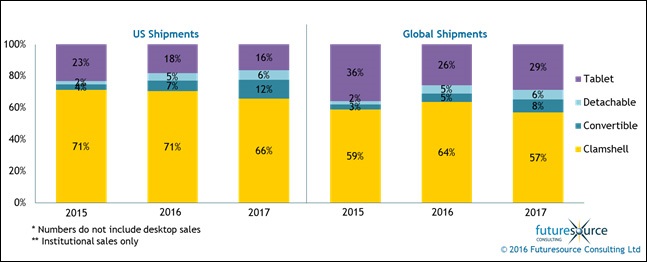

The prognosticators at Futuresource, meanwhile, are bullish on 2-in-1 devices, or devices with detachable or convertible keyboards that can be used either as a traditional laptop, or as a tablet. That subsector is expected to increase in the U.S. market from 6 percent of the total shipments of non-desktop PC devices in 2015 to 18 percent in 2017.

The strength of the 2-in-1 devices is their “form factor” says Fisher. Their ability to accommodate apps that encourage tactile interactions with touchscreens as well as traditional efficiency of word processing and research on a keyboard makes the flexible devices “almost ideal” for the education market, he says.

In an added bonus for re-sellers, the growing preference for the slightly more hardware-intensive 2-in-1 devices is likely to slow the drop in price points for the market overall.

While Microsoft might traditionally be expected to be best positioned to capitalize on the 2-in-1 market, Google’s operating systems are outperforming expectations across the board in the U.S. K-12 education market, including in the battleground for 2-in-1 devices.

Google continues to capture market share: 57 percent of U.S. educational devices sold run on the company’s operating system, up from 51 percent during the third quarter last year. Their growth comes at the expense of both Microsoft and Apple, said Fisher.

Despite the negative global outlook for 2016, Futuresource expects the market to bounce back in 2017, and grow at a 19 percent rate over the dip this year.

See also:

MediaBox HD is the Where you can stream all Netflix, Amazone Prime and HBO movies and TV Show without any subscription. MediaBox HD provides high speed server link so you can enjoy the movies and TV show wothout any buffering. MediaBox HD suppot in Android as well as IOS users.

Watch IPL 2020 live all matches on LivenetTV APK.

An impressive share, I just given this onto a colleague who was doing a little bit evaluation on this. And he in reality ordered me breakfast due to the fact I discovered it for him.. smile. Consequently allow me alter that: Thanks for the deal with!